By PelMon Wealth Management | Topic: Retirement Planning | Reading Time: 6 minutes

The Most Consequential Retirement Decision Most Canadians Underestimate

When should you start taking your Canada Pension Plan? It sounds like a simple administrative question. It is not. The age at which you begin collecting CPP is one of the most financially significant decisions you will make in retirement — and it is permanent.

Get it right and you could receive tens of thousands of dollars more over your lifetime. Get it wrong and there is no reversing it.

Here is what the numbers actually tell you.

How CPP Works — The Basics

The Canada Pension Plan is a contributory, earnings-related pension that almost every working Canadian pays into throughout their career. The amount you receive is based on how much you contributed and for how long — not a flat rate.

The average CPP benefit in 2025 was $803.76 per month. The maximum amount a new recipient could receive starting at age 65 is $1,507.65.

The gap between the average and the maximum is significant — and it reflects the reality that most Canadians have years of lower earnings, part-time work, or career gaps in their contribution history. Before making any decision about when to take CPP, log into your My Service Canada Account and get your personal estimate. Do not assume you will receive the maximum.

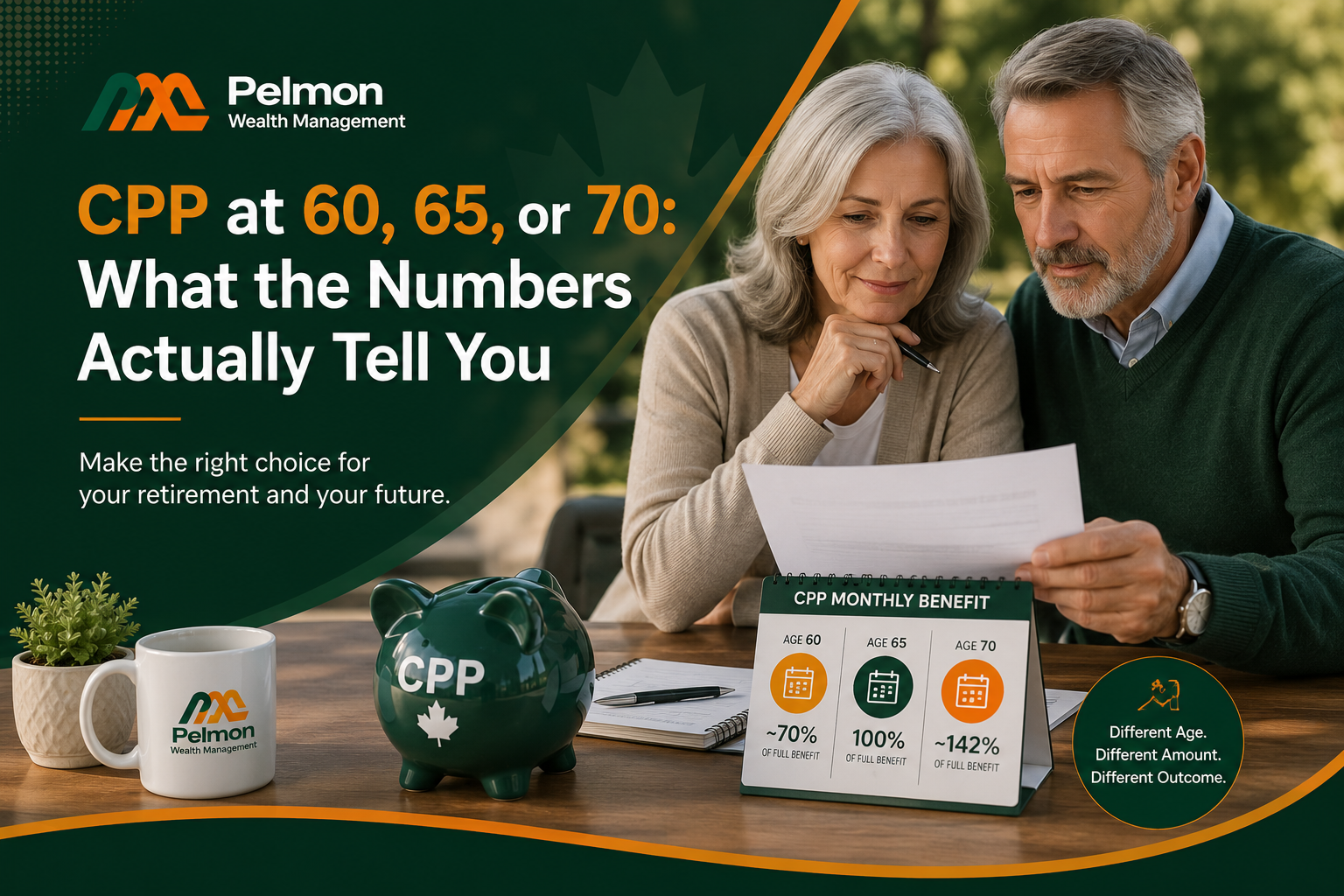

The Three Ages — and What Each One Costs or Gains You

You can start taking CPP as early as age 60, but you will lose up to 36% of your pension permanently if you take it that early. CPP payments are reduced by 0.6% for every month before your 65th birthday. If you delay receiving your CPP until age 70, your payments will be permanently increased by 0.7% for every month after your 65th birthday — 8.4% per year.

In concrete terms for 2026:

The maximum CPP at age 65 in 2026 is $1,507.65 per month. Taking it at 60 reduces it 36% to $964.90 per month. Deferring to 70 increases it 42% to $2,140.86 per month.

That is a difference of $1,175.96 per month — or $14,111.52 per year — between taking CPP at 60 versus waiting until 70.

The Break-Even Analysis: When Does Delaying Actually Pay Off?

The break-even age for taking CPP at 60 versus 65 is approximately age 74. The break-even for delaying from 65 to 70 is approximately age 82.

What this means practically: if you start CPP at 60 and live past age 74, you would have received more total lifetime income by waiting until 65. If you delay from 65 to 70 and live past age 82, the higher payments more than compensate for the five years you went without CPP income.

The average 60-year-old Canadian can expect to live to roughly 84 to 86, which means most people come out ahead by waiting — but only if their personal financial situation allows for it.

The break-even analysis is a useful framework, but it is not the only consideration.

The Case for Taking CPP at 60

Taking CPP early is not always the wrong decision. There are situations where it makes clear practical sense:

- You have a serious health condition or shortened life expectancy

- You have no other income sources and need cash flow immediately

- You want to avoid drawing down your RRSP or TFSA early

- You plan to invest the CPP payments and are confident you can generate a return higher than the 7.2% annual equivalent that delaying provides

A reduced CPP is infinitely better than credit card debt at 20% interest. Some retirees also take CPP at 60 specifically to invest it, betting they can earn more than the 7.2% annual equivalent the delay would have provided.

The Case for Waiting Until 65

Age 65 is the standard starting point for a reason. You avoid the 36% permanent reduction, you qualify for Old Age Security at the same time — which simplifies your income planning considerably — and you have not needed to fund five years of living without CPP income.

For most healthy Canadians with other income sources or savings to draw on, 65 remains the most straightforward choice.

The Case for Deferring to 70

If you are healthy, still working, and have sufficient income or assets to bridge the five years between 65 and 70, deferring CPP is often the most financially advantageous decision.

The 42% increase is guaranteed, inflation-adjusted, and lasts for the rest of your life. No investment can offer that combination of certainty and return.

During those years you are not collecting, the investment and inflation risk is the government’s problem, not yours.

One important consideration: if your total net income exceeds roughly $90,997 in 2026, you begin losing 15 cents of OAS for every dollar above that threshold. CPP payments count toward that income, so a large CPP benefit combined with RRIF minimum withdrawals and workplace pension income can push you into clawback territory. This is a critical tax planning consideration that is often overlooked.

The Decision Is Personal — Not Universal

There is no universal best age. The math favors delaying past 65 if you live past roughly age 74. The math favors claiming at 60 if you expect a shorter life or need the income now.

The right answer depends on your health, your other income sources, your tax situation, your spouse’s income and CPP entitlement, and your broader retirement plan. This is not a decision that should be made based on what a friend or family member did.

Talk to a Financial Advisor Before You Decide

The CPP decision is permanent. A financial advisor can model out the exact numbers for your personal situation — including the interaction between CPP, OAS, RRIF withdrawals, and any workplace pension you may have — and help you choose the timing that maximizes your lifetime retirement income.

Book a free consultation at penejoh@pelmon.ca or call (204) 590-5272.

Sources: Canada Life, CPP Payment Dates and Amounts; Service Canada, CPP Maximum Benefit Amounts 2024–2025; LifeMoney.ca, CPP at 60 vs 65 vs 70 Break-Even Calculator 2026; Wealthsimple, CPP Retirement Pay Dates 2025; Wealthvieu, CPP Benefits 2026 Guide